how to compare trading strategies

Last Updated on June 24, 2022

What are the common types of futures trading strategies? Here is a list:

- Calendar Spreads – Spreading the same future, but of different termination dates

- Spreading 2 different futures to switch relative value

- Spreading a future and its underlying asset

- Spreading 2 similar futures that are listed on different exchanges

- Diffusive unregulated futures

We volition review each of these strategies and give them a score.

Scoring Criteria:

- Profitability

- This refers to latent winnings if you manage to carry through the patronage

- Ease of implementation

- This refers to how available information technology is to execute the trade Eastern Samoa an individual retail trader

- Complexity of trade

- Obvious

Not-unusual futures strategies

The following are strategies not specific to futures, but can live through with futures. We will not cover them therein article.

- Trading futures directionally and for purchase. This is celebrated as trading in an instantly way.

- Trading futures because the trader has no approach to the underlying

- Because the underlying is not tradeable. Eg. Temperature futures

- Because the trader has geo-political limitations

Before we can talk active scheme, let's do a quick summary of what futures are. You bum skip the next part if you are acquainted futures.

What are futures?

Official definition: A futures cut is an obligation to buy or sell an asset at a certain price and clock time.

This substance that a hereafter contract will order that Trader X will buy Asset A at Price B from Trader Y at Time C.

Trader X buys a tense from Trader Y.

Dealer Y is able to sell (AKA short) this future without first owning IT. This is because selling a tense is simply an agreement to trade a certain asset in the future.

Asset A is acknowledged as the underlying asset, besides known as the spot. (We will use the terms, underlying asset and spot interchangeably.)

Price B is the Leontyne Price of the future.

Prison term C is the expiration date of the future.

If you buy a coffee coming contract, which expires in 6 months, at $105, it is an obligation to buy the underlying burnt umber product at $105 in 6 months' time. The trader who sold you that same future at $105 is duty-bound to sell you the underlying coffee product at $105 in 6 months' time.

Thus, you can repute a future as a production whose price is dependent on its underlying plus.

Expirations

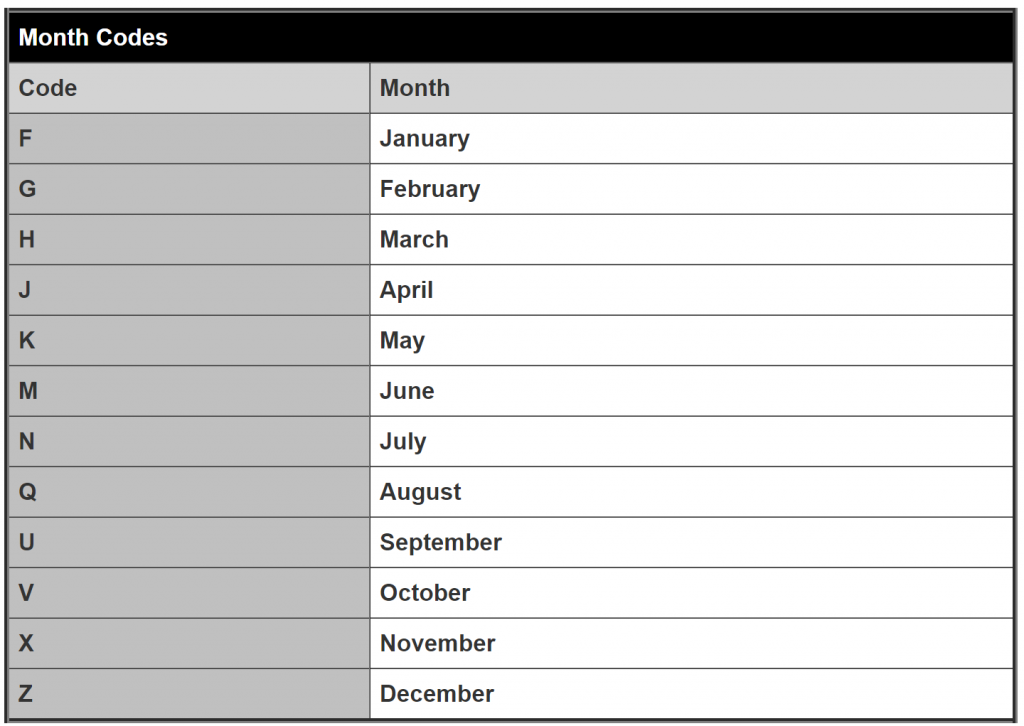

Futures have expiration dates. The name of the future will let in the expiration calendar month and year.

Eg. The shortname for the Three-Month EURIBOR Futures that is listed on the Worldwide Exchange (ICE) is I.

IU19 means that this I abridge expires on September 2022.

I H22 means that this I contract expires on March 2022.

The letters U and H represent the month. The numbers pool represent the year.

How do I love which month the letters in the name refer to? Refer to this heel.

This calendar month code is standardised across all futures products (bonds and another plus classes).

Once the futures expire, 2 things can happen.

- Exchange of goods – If you bought a coffee future, you are now obliged to receive physical coffee berry from the seller of that futures. Congrats you are screwed.

- Cash-settled futures – Some futures put on't require somatogenic delivery of goods. You pay (or get paid) the remainder between the prevailing underlying price and the price antecedently agreed upon.

Let's use the previous example where the deal out happened at $105 and acquire that the deep brown future is cash-settled. If prices nowadays are at $110, then the purchaser of that future profited $5 from the seller. The seller will remuneration the buyer $5 when the future expires and follow through with it.

How to trade futures?

Trading futures involves taking advantage of the unique features of futures: 1) Futures expiry dates 2) Futures Rollovers and 3) Futures and their underlying assets.

Permit's cover this list of strategies one by one:

- Calendar Spreads – Spreading the same future, but of different departure dates

- Spreading 2 assorted futures to trade relative value

- Spreading a future and its underlying asset

- Diffusive 2 similar futures that are traded on different exchanges

- Spreading unregulated futures

Wait, what does spreading mean? IT simply means to tall unmatched asset and short another.

Olibanum, when I say "Spreading a early and its underlying asset", I mean to overnight the future and short the subjacent plus, or vice versa.

» To live trading futures (live or demo), watch out this guide: Synergistic Brokers Python API (Native) – A Step-by-step Guide

Scheme 1: Calendar Spreads – Spreading the same future, but of different expiration dates

Buying unmatched future of a certain expiration date and selling other of a contrasting expiration appointment is titled a calendar spread.

This spread is called an intra-cut circularise arsenic we are trading the same future of different expiration dates.

To better understand this strategy, we will look at a real-life example.

Case Study: Euribor Calendar Spreads and Butterflies

Asset background

- Asset: Deuce-ac-Month Euribor Futures (Shortname: I)

- Inside information: Link to product specifications

- Telephone exchange: Intercontinental Switch over (ICE)

- Opportunity in this strategy: This scheme creates a constant mean-reverting price structure.

The Euribor future is priced supported on the Euribor (you father't order).

Official definition (from Wikipedia): The Euro Interbank Offered Rate (Euribor) is a daily reference rate, promulgated by the European Money Markets Bring,[1] based on the averaged interest rates at which Eurozone Banks proffer to contribute unsecured finances to other banks in the euro wholesale money market (or interbank market).

In obtuse English: It is the average interest rate European banks charge for each one other for shortstop full term loans.

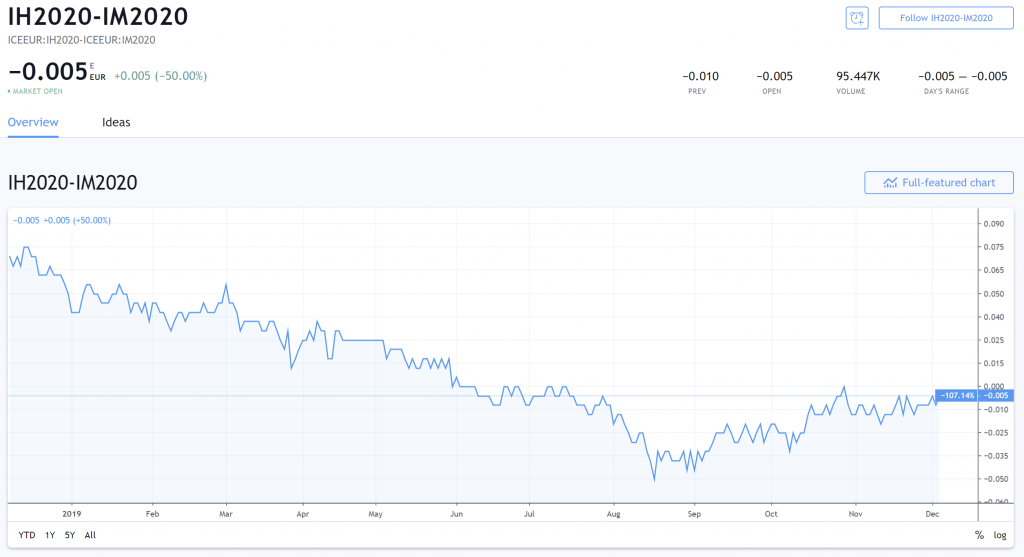

The Three-Month Euribor Futures expiring in Vitiat 2022 is called the IH2020 contract. The I stands for the futures name, H tells America that the contract expires in March, and 2022 tells United States of America information technology expires in 2022.

IH2020 can equal written as IH0. IH2021 can be written as IH1 and so on.

IH0 stool be interpreted Eastern Samoa IH2010 or IH2030. But judging that we are in 2022 (A of this writing), it is understood that IH0 refers to IH2020.

Price vs Expected Pursuit Rates

The cost of a Three-Calendar month Euribor Future is inverse to interest rates.

It is approximated as 100.00 minus the expected pursuit rate [1] (at the time of the futures expiration).

So, if the Euribor range is expected to embody 2% at March 2022. IH2020 should beryllium trading around 100 – 2 = 98.

Since the rates in Europe are electronegative, the chart above shows the IH2020 is trading at 100.41 (calculated from 100 – (-0.41)).

Understanding Calendar Spreads

When we buy an IH0 contract and deal an IM0 (expires in June 2022) contract, we are effectively longing a calendar spread of H0M0.

On the other hand, when we sell an IH0 contract and buy an IM0 concentrate, we are effectively shorting a calendar spread of H0M0.

When we extendible a H0M0 spread, we are essentially card-playing that the Euribor in June 2022 bequeath procession (remember, when rates rise, future prices fall) compared to the Abut 2022's rate.

In other words, we are sporting that the Leontyne Price difference 'tween IH0 and IM0 will narrow. If we short H0M0, we are betting that the price different will widen.

Mix and twin spreads

You hindquarters think of a H0M0 spread as an exposure to 3 months' deserving of Euribor risk.

Similarly, a H0H1 broadcast essentially contains 12 months' worth of Euribor risks.

Spreads can be mixed and matched to equate to each different.

A H0H1 spread is equivalent to a H0M0 + M0U0 + U0Z0 + Z0H1 structure A each of the 4 last mentioned spreads consists of 3 months' worth of risks from each one.

There are other slipway to recreate a H0H1 complex body part:

- H0U0 + U0H1 (6 months + 6 months)

- H0M0 + M0H1 (3 months + 9 months)

- H0Z0 + Z0H1 (9 months + 3 months)

This knowledge is functional for us when we want to rotate our positions, and IT is important for USA to see the next part – Euribor Butterflies.

Euribor Butterflies

We are in conclusion talking about the veridical scheme.

What perform you think the following structure represents?

H0M0 – M0U0 (note that previously we were adding the 2, immediately we are minusing)

H0M0 – M0U0 can be handwritten as H0 – 2*M0 + U0.

Look at that beautiful thang!

If you don't know what's the trade to terminat for this price behaviour, you buttocks appressed this tab now and go learn another profession.

The chart above represents a Euribor Coquette. (And no, this is not the same American Samoa an option butterfly.)

When we polysyllabic H0 – 2*M0 + U0, we are long 1 contract of H0, short 2 contracts of M0 and long 1 contract of U0.

We are essentially dissipated that the Euribor rates in June 2022 testament rise congener to March on 2022 and September 2022.

Hedge and Risk Exposure

If H0M0 + M0U0 has 6 months of Euribor exposure, how much exposure does H0M0 – M0U0 have?

The solvent is ZERO!

The beautiful matter about the Euribor butterfly is that it is hedged to almost everything! You don't even hold any net Euribor exposure.

Information technology is hedged to almost macroeconomic events, to stock market movements, to the country's economic conditions, currency risks, to the credit military rank up or downgrade of organized bonds, tweets from politicians etc.

This means that you tooshie log Z's well at dark.

This structure consists of futures of 3 different expirations. We can go one step further and build structures consisting of 4 or more expirations.

Why trade future butterflies

The axiomatic answer is to swop the butterfly's mean reverting conduct.

But if we break IT down, there are 2 ways to trade this:

- Use it to bet on future Euribor price change

- Mean retrovert it by executing the butterfly at trade good prices

Method 1:

This was what we spoke most when we mentioned that longing a H0 – 2*M0 + U0 butterfly is essentially betting that the Euribor rates in June 2022 will rise up relation to March 2022 and September 2022.

Method acting 2:

The mean regression deal looks obvious only it is hard to execute.

Here your trading edge is that you posterior enter the individual contracts at better prices than the other market players.

In the above chart, you want to long the butterfly at the green lines and short at the scarlet lines.

But but… the prices didn't regular hit those areas, how is that possible?

2 reasons:

First, the prices to a higher place are from the destruction-of-solar day. This means that there are opportunities to get prices nearer to the red and green lines if we flavour at the intra-day price information.

Second, remember that this chart is made up of 3 separate futures (H0, M0 and U0). The lazy and inutile way to enter these 3 legs is to live a price taker (i.e. buy out at the ask price and sell at the press price).

If we enter apiece patronage at slightly better prices than simply being a price taker, you'll end up with prices nearer to the red and light-green lines.

That said, if you are a lazy trader, you give the sack still be profitable A long as you are patient and wait for the prices to diverge off the beaten track off the mean.

Separate butterflies

In our pillowcase subject, we utilised Euribor futures as our asset class, but in that location are other worry rank and non-interest assets (care commodities) we can trade.

Here is a list of rate of interest products: STIR Futures

Ending notes for Strategy 1

We've only concisely talked about the basics of the butterfly strategy. The devil lies in the details.

The persuasiveness of this strategy is the dealer's execution prowess and plus extract.

There are risks for this strategy too. Most of it comes of black swan risks and poor execution, but there are ways to palliate those.

Strategy 1 Grades

- Profitability (5 points = Very Profitable): 4/5

- Ease of execution (5 points = Very Difficult): 4/5

- Complexity of trade (5 points = Very Complex): 3/5

Strategy 2: Disseminative 2 different futures to trade relative note value

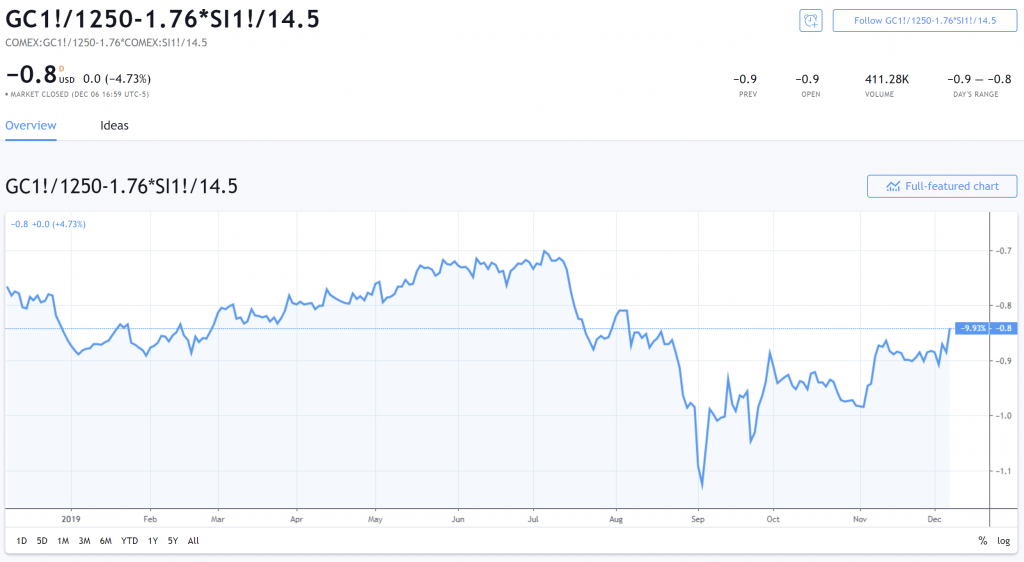

When we womb-to-tomb Gold and short Silver, we are said to own monthlong a Metal-Silver cattle farm. We are betting that Gold rises relative to Silver.

This is called a relative value trade, as we are not attentive with the absolute price behaviour of Gold (or Silver). We are only preoccupied about how Gold rise or fall relative to Silver.

These spreads are titled inter-contract spreads as we are trading 2 separate contracts.

The above shows the cattle farm between Gold and Silver Futures. Hedged by contract value as of now (8th December 2022).

Spreading to target specific risk exposures

Another way to think about relative value trading is to target specific risks.

Spreading between 2 distinct futures allows to duck against outcaste exposures and keep down specific exposures.

Case: Public exposure 2 hypothetical stocks

Have's say we believe Stock X has better technology than its competitors. We want to make a abundant bet on its tech.

In this case, we require to take back a risk on Stock X's tech prowess.

Just Stock X is to a higher degree righteous its technical school, it includes trading operations, management, marketing, stock exchange influence and other factors. If we long Stock X, we will essentially be taking a calculate on those other factors too.

The solution? Hedge inaccurate the unwanted factors (i.e. hedge away unwanted risk)

We discovery a stock that is similar to Stock X in every way leave out its tech. Let's call this Stock Y.

And we short Stock Y.

The final deal out is to long Stock X and fugitive Stock Y. To put this in mathematics form:

Stock X – Stock Y = (A+B+C) – (A+B-D) = C – D

Where A, B, C, D are factors and C and D represent the tech of Stocks X and Y severally.

Now, you're left with C-D, which is the difference betwixt the tech power of Stock X and Y.

This is the targeted risk we wish.

Hedging Ratios – How much to long and stubby

The short serve is, you neediness both assets of your spreads to move the same amount when the hedged photo moves.

I'll write a separate blog post on scheming hedging ratios.

Essentially, you want to be immune to the hedged exposure.

Example 1: Oblong Stock A and short Stock B

Both Stock A and B are correlated to the widespread securities market. This means that when the Sdanamp;P500 moves, Stock A and B will motility excessively.

How much Stock A and B move is proxied aside a measured called commercialize Of import. Beta measures the sensibility of a stock price change to the relevant general market's change.

If Stock A's beta is 1.5, this means that it moves 1.5% when the market moves.

(p.s. Beta is a generic wine metric premeditated from existent data. The value of the betas changes over time should only be used as an approximation.)

When we spread Stock A and B, we are trying to hedge absent food market risk.

To do that, we may enter much positions of the Stock with the lower beta and less of that with the higher beta.

Thus, if Stock A's beta is 1.5 and B's explorative is 2, we long 4 shares of A and curtly 3 shares of B. (Math: 4 x 1.5 = 3 x 2)

Example 2: Elongate Bond A and unmindful Bond B

There are nobelium betas in bond. But there is duration.

Length is a metric that measures the sensitivity of the price of a bond to a change in interest rates.

You can think of duration as the equivalent of beta for bonds.

Similarly, buy much of the bond with turn down beta and less of that with higher beta.

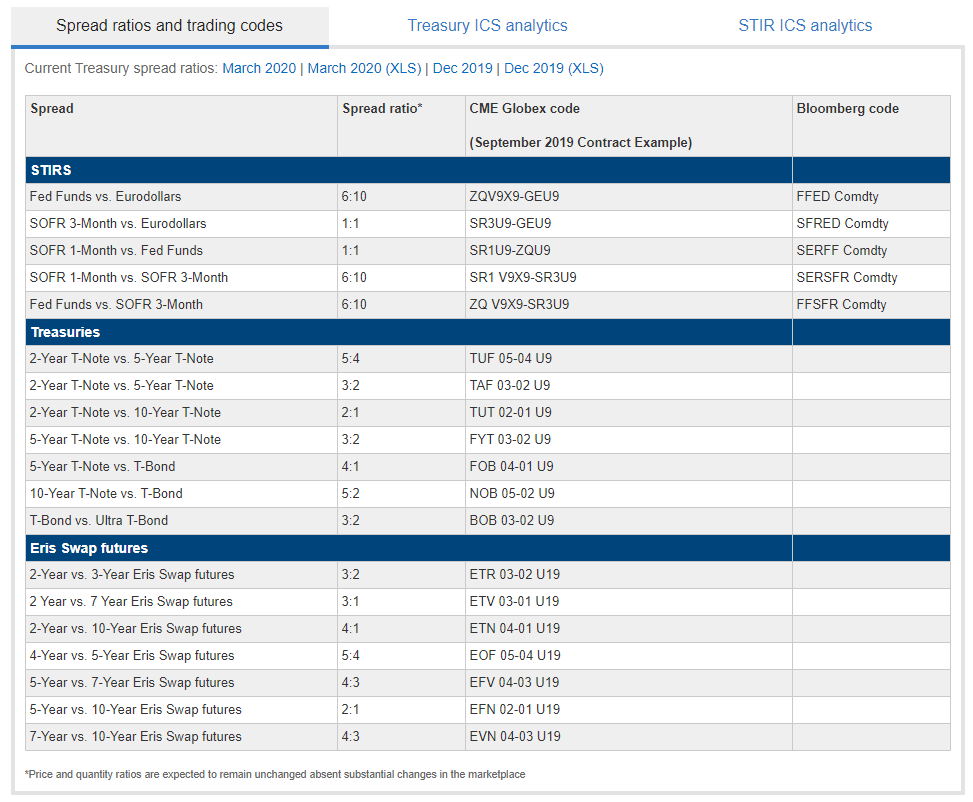

Common Futures Spreads

Here is a name of common inter-contract futures spreads:

These spreads consist of 2 assets.

However, we can bestow more assets to our spreads. The Sir Thomas More assets, the more unfluctuating the price behaviour of the spreads.

One example of a 3-three-legged anatomical structure is to long the 2-twelvemonth, insufficient the 5-year and long the 10-year Treasuries in a continuance-neutral fashion. This is similar to our intra-contract bridge butterflies in strategy 1.

Strategy 2 Grades

- Profitableness (5 points = Selfsame Profitable): 2.5/5

- This has less to do with the spread and more with your understanding on the fundamental products

- Relaxation of execution (5 points = Really Difficult): 1/5

- Complexity of barter (5 points = Very Complex): 2/5

Scheme 3: Spreading a future and its underlying asset

A futures contract is based on an underlying asset (AKA daub).

The futures concentrate and the spot are priced equally on the future's going date, but they are usually not priced equally star up to the expiration date.

The introductory idea of the trade

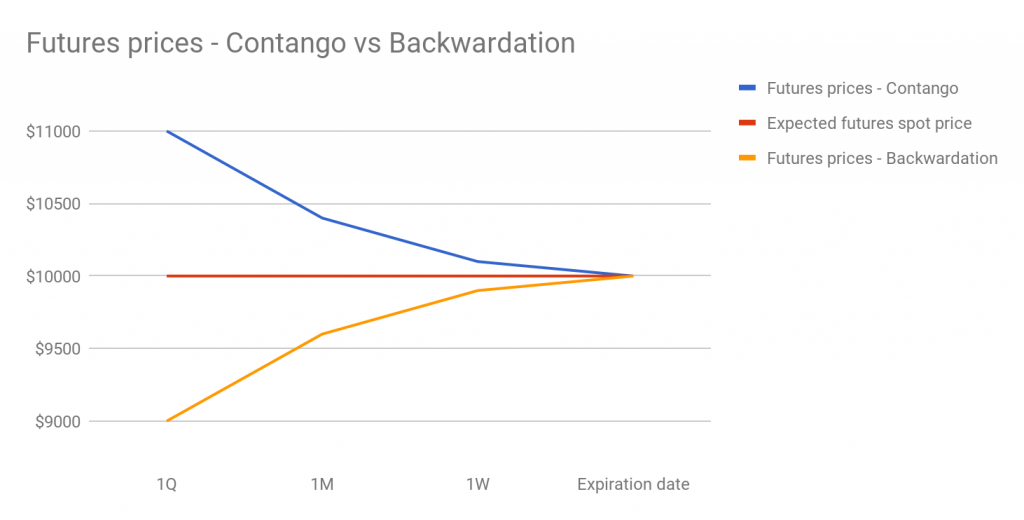

When the futures' price is higher than the espy price, it is said to embody in contango.

In contango, you desire to short futures contract and prospicient the spot leading up to the expiration date. This is known as a payment-arbitrage.

When the futures' price is depress than the spot price, it is said to be in average backwardation (commonly famed as retributive backwardation).

In backwardation, you want to endless futures narrow down and short the spot up up to the expiration date. This is known as a reverse payment-arbitrage.

Reasons of Contango and Backwardation

Reasons for contango

- Increasing future demand for the underlying

- With higher future demand, the future declaration which settles in a later date, leave be more desired. More demand leads to more buyers and a high price for the futures.

- Abrupt increase in add of the inherent

- More supply leads to lower current spot monetary value.

- Toll of storing of the underlying plus is positive

- If the underlying needs a come in to be stored, there is a cost related to with this storage. Eg. If our coffee future expires 6 months later, there is a "theoretical" storage cost to hold the physical coffee bean for 6 months. This causes the future damage to constitute somewhat high than the maculation.

Reasons for backwardation

- Decreasing future require for the inexplicit

- With lower future involve, the future contract which settles in a later date stamp, will be less in demand. Less demand leads to less buyers and a lower price.

- Sudden decrease in supply of the underlying

- Inferior supply leads to higher current spot price.

- Cost of storage is negative (i.e. the is interest to follow earned by storing the goods)

- Sometimes the stored goods can produce positive yield for the person WHO holds the goods. This is noted as convenience yield. Eg. Retention oil power help one profit when there is a sudden supplying crash or He bathroom use it in some output process.

Risks of Cash-And-Carry-Arbitrage

Strictly speaking, an arbitrage is a risk free-soil trade that takes reward of a mispricing betwixt 2 like assets.

All the same, the cash-and-carry arbitrage is non risk free.

Here are some risks or factors that diminish this trade's profitability:

- Cost of yearning or shorting the situatio is not zero. These costs power follow equal to Oregon much the profit from the arbitrage

- Increase in gross profit margin requirements for futures

- Sudden demand or provision shock mightiness causal agent a margin birdcall

- Liquidity risks

Scheme 3 Grades

- Profitability (5 points = Very Profitable): 1/5

- This strategy is too obvious.

- Ease of execution (5 points = Very Difficult): 1/5

- Complexness of trade (5 points = Very Hard): 1/5

Scheme 4: Spreading 2 mistakable futures that are listed connected different exchanges

This strategy involves longing one future and shorting a similar one on another exchange.

Army of the Righteou's use gold as an instance. Gold is listed on multiple exchanges.

If a gilt future is traded at a lower price along COMEX and at a high terms happening TOCOM (accounting for vogue differences), we elongate Gold on COMEX and short IT on TOCOM.

Reasons for futures mispricing

Mispricings come up between different exchanges as there might be restrictive controls at certain exchanges (eg. daily price act upon limits), take or supply shocks in one body politic, different trading multiplication, and the lag in the transfer of news.

Arbitrage Risks

Your risks will involve up-to-dateness movements, capital controls, limitations over the transfer of goods.

Strategy 4 Grades

- Profitability (5 points = Very Profitable): 1.5/5

- The strategy is too obvious and competitive.

- Ease of execution (5 points = Very Difficult): 5/5

- Any opportunities left are hoarded by squeaking-frequency hedge funds.

- Complexness of trade (5 points = Very Complex): 1/5

Strategy 5: Dispersive Unstructured Futures

Unregulated futures are products that behave like futures, but they are not listed happening conventional futures exchanges.

The most common typewrite of unregulated futures is in the cryptocurrency market.

The biggest crypto futures exchange is BitMex (as of today, Dec 2022).

Unregulated futures are more often than not Sir Thomas More inefficient and have much mispricings compared to traditional futures (partly due to possible securities industry manipulation).

Thus, by favorable the first 4 strategies listed in this clause and applying them to these unregulated futures, there is potential difference for net.

Since these futures are not ordered, IT is kinda a wild west. In that respect are opportunities for profits just you might comprise draw sucker-punched and turn a loss money too.

Make amusing in these markets, but do make sure it is legal to trade wind these unregulated futures in your country!

Strategy 5 Grades

- Profitability: ??

- Ease of execution: ??

- Complexity of trade: ??

What platform OR broker should I use for futures trading?

I Shan't do a flooded review here but here is a list of brokers for retail traders:

Interactive Brokers – Lowest commissions

TD Ameritrade – Best trading platform

TradeStation – Smashing platform, competitive rates

Charles Schwab – Unequalled order types

E*TRADE – Well-watermelon-shaped offering

Source: stockbrokers.com/guides/futures-trading

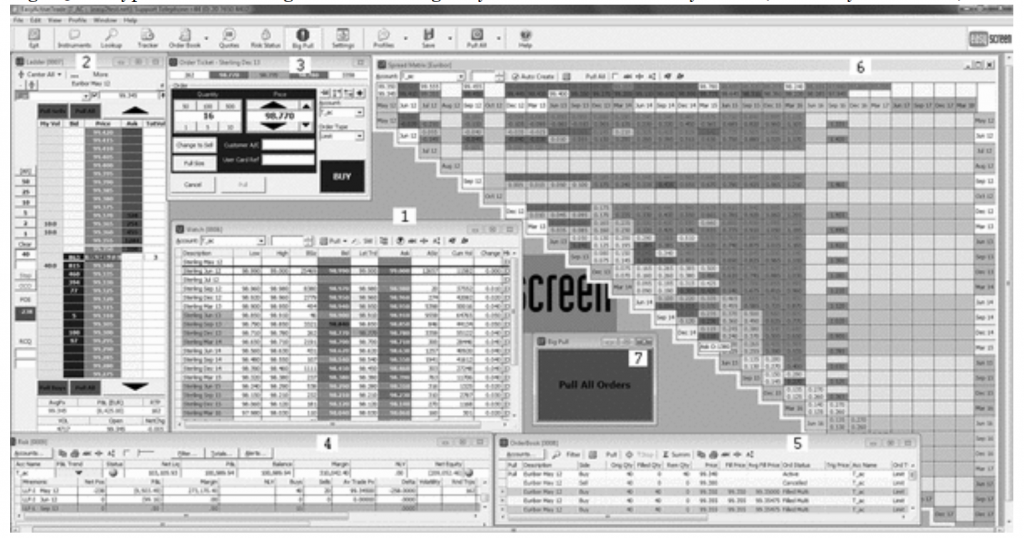

What does a professional futures trader computer screen look like?

A futures trader might have 4 to 8 computer screens.

This is how a master futures trader's typical shield will look like, peculiarly if you are diffusing intra-narrow down futures.

Related Questions

How much coiffe you pauperization to craft futures?A ballpark number is $10,000. Every futures trade requires you to set up money for margin. You need sufficiency capital to 1) enter your trades with proper sizing position sizing, 2) buffer for losses and 3) maintain an account minimum.

This article bequeath be useful: "Minimum Superior Needed to Start Solar day Trading Futures"

How to price futures? The academic answer is: Futures Price = Spot Toll × (1 + Risk-Free Interest Charge per unit – Income Yield).

More info here: Futures Pricing (Wikipedia)

This article is non financial advice!

how to compare trading strategies

Source: https://algotrading101.com/learn/futures-trading-strategies-guide/

Posted by: ownbysporrok1944.blogspot.com

0 Response to "how to compare trading strategies"

Post a Comment